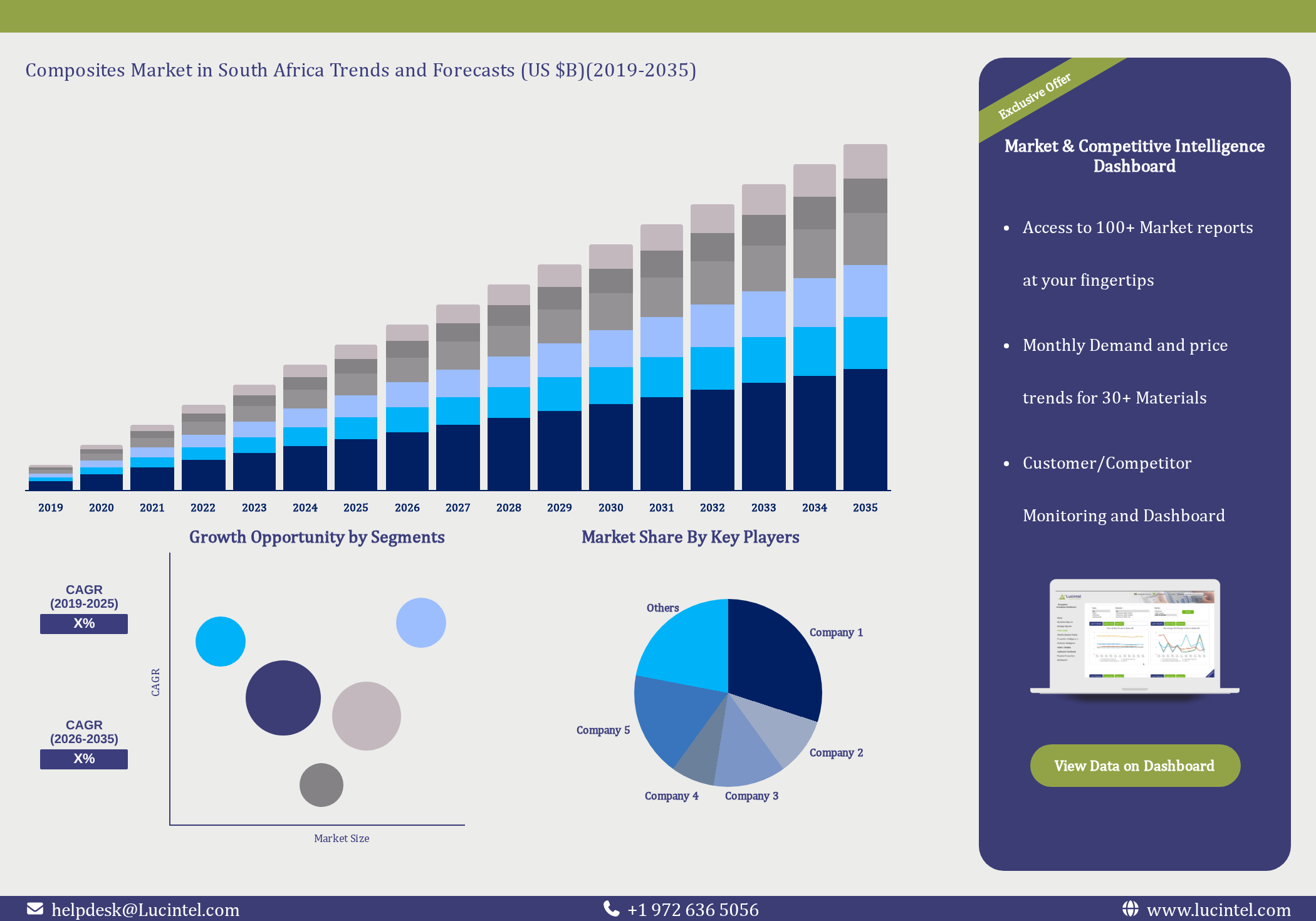

Composites Market in South Africa Trends and Forecast

The future of the composites market in South Africa looks promising with opportunities in the PAN based carbon fiber and PITCH based carbon fiber markets. The global composites market is expected to reach an estimated $70 billion by 2035 with a CAGR of 4.1% from 2026 to 2035. The composites market in South Africa is also forecasted to witness strong growth over the forecast period. The major drivers for this market are growing demand in automotive and aerospace sectors for lightweight, high-strength materials drives composites adoption to improve fuel efficiency and reduce emissions, expansion in construction, wind energy, and marine sectors boosts composites use due to corrosion resistance, durability, and long service life and innovations in resin systems, fiber reinforcement, and processes like injection molding and automated layup enhance performance, reduce costs, and expand composites applications.

• Lucintel forecasts that, within the end use industry category, transportation will remain the largest segment over the forecast period as growing demand for lightweight, fuel-efficient, and low emission vehicles is driving composite adoption in transportation. Composites reduce vehicle weight, improve performance to meet stringent emission regulations.

• Within the carbon fiber type category, pAN based carbon fiber will remain the largest segment due to the demand for ultra-lightweight, high-strength materials is driving PAN based carbon fiber growth due to its superior stiffness, fatigue resistance, and high performance-to-weight ratio.

Emerging Trends in the Composites Market in South Africa

The composites market in South Africa is undergoing rapid transformation as manufacturers, end users, and policymakers seek lighter, stronger, and more sustainable materials. Rising infrastructure investment, automotive localization, and renewable energy deployment are accelerating demand for advanced composite solutions. At the same time, local supply chain constraints, skills gaps, and cost pressures are shaping how innovations are adopted. New applications in transport, construction, and energy are expanding the addressable market, while digital design and automation reshape production processes. Together, these forces are redefining competitiveness and creating new growth pathways in the composites market in South Africa.

Recent Developments in the Composites Market in South Africa

The composites market in South Africa is undergoing notable transformation as manufacturers, end users, and policymakers converge around lightweight, durable, and sustainable materials. Growth is being propelled by infrastructure renewal, transport modernization, and the emergence of local value chains linked to global OEMs. Recent developments span bio-based innovations, capacity expansions, new regulatory drivers, and digital manufacturing practices. Together, these shifts are redefining performance benchmarks, cost structures, and competitive dynamics, while creating new opportunities for South African firms to integrate into high-value regional and international supply networks.

Strategic Growth Opportunities for Composites Market in South Africa

The composites market in South Africa is entering a pivotal growth phase, supported by industrial diversification, sustainability priorities, and infrastructure modernization. Local manufacturers are increasingly shifting from traditional materials such as steel, aluminum, and concrete toward lighter, stronger composite solutions. Government investments in transport, energy, and housing, combined with global supply chain reconfiguration, are opening new opportunities across end-use applications. Five strategic growth avenues stand out for investors and producers, each offering potential to scale volumes, deepen localization, and enhance South Africa’s competitiveness in regional and global composite value chains.

Composites Market in South Africa Driver and Challenges

The composites market in South Africa is influenced by a mix of technological, economic, and regulatory dynamics that shape demand across construction, automotive, renewable energy, and aerospace sectors. Advancements in materials science, lightweighting trends, and decarbonization policies are expanding application possibilities, while local industrialization goals encourage domestic production and value addition. At the same time, cost pressures, skills gaps, and standards compliance requirements add layers of complexity. Understanding the main growth drivers and structural challenges is essential for assessing long‑term opportunities and strategic positioning within South Africa’s evolving advanced materials ecosystem.

The factors responsible for driving the composites market in South Africa include:

The challenges in the composites market in South Africa are:

Combined, the growth drivers and structural challenges create a complex but promising outlook for the composites market in South Africa. Infrastructure expansion, renewable energy growth, industrial applications, and supportive industrial policy are steadily increasing demand for advanced composite solutions. However, high input costs, skills shortages, and regulatory hurdles continue to moderate adoption and concentrate opportunities among better‑resourced players. Stakeholders that invest in local raw material supply, workforce development, standards alignment, and end‑user education will be best positioned to unlock sustainable, long‑term value within South Africa’s composites value chain.

List of Composites Market in South Africa Companies

Companies in the market compete on the basis of product quality offered. Major players in this market focus on expanding their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. Through these strategies, composites market companies cater to increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the composites market companies profiled in this report include:

Composites Market in South Africa by Segment

The study includes a forecast for the composites market in South Africa by end use industry, manufacturing process, molding compound, resin type, fiber type, fiber glass product form and carbon fiber type.

Features of the Composites Market

Article

Composites Market in South Africa: How Are Advanced Materials Rewriting Industrial Strategy?

Dallas, June 4, 2026 – The composites market in South Africa is moving from niche engineering material to strategic enabler for the country’s energy, mobility, construction, and technology ambitions. As domestic manufacturers seek lighter, stronger, and more durable solutions, composite materials are reshaping competitive dynamics across sectors ranging from wind energy and rail to telecoms infrastructure and consumer electronics. This article examines the major trends, the sectors most impacted, the challenges and opportunities ahead, and the emerging use cases in the technology industry, alongside recent developments that signal where the market is heading.

What Major Trends Are Redefining the composites market in South Africa?

Several converging shifts are changing how South African companies specify, design, and source composite materials. These shifts reflect both global innovation and local industrial policy priorities, including localization, energy transition, and infrastructure resilience.

Which Sectors Will Feel the Strongest Impact from These Composite Innovations?

The composites market in South Africa is not evolving in isolation; it is tightly intertwined with strategic sectors that underpin growth and job creation. The most pronounced disruption is expected in energy, transportation, construction, and technology-linked manufacturing.

How Will These Trends Disrupt Competitive Dynamics Across Industries?

The rise of advanced composites is altering cost structures, supplier relationships, and product strategies in the composites market in South Africa. Companies that adapt quickly can reposition themselves as solution providers rather than commodity suppliers.

What Key Challenges Could Slow the Momentum of the composites market in South Africa?

Despite strong structural drivers, the composites market in South Africa faces practical and strategic barriers that could constrain its trajectory if not addressed through coordinated industry and policy action.

Where Do the Biggest Opportunities Lie for Stakeholders in South Africa?

For investors, industrial groups, and policymakers, the composites market in South Africa presents a portfolio of opportunities that align with national development priorities and emerging export niches.

How Is the Technology Industry Using Composites in South Africa?

The technology ecosystem is a rapidly evolving frontier for the composites market in South Africa, as hardware, connectivity, and advanced manufacturing converge.

What Recent Developments Signal the Future Direction of the composites market in South Africa?

Recent project announcements, partnerships, and technology deployments provide early indicators of how the composites market in South Africa is likely to evolve over the next few years.

How Should Businesses Position Themselves as the composites market in South Africa Matures?

Strategic positioning in the composites market in South Africa will require a blend of technology choices, ecosystem partnerships, and long-term capability-building. Companies that treat composites as a core competency rather than a peripheral material category are likely to outperform.

The composites market in South Africa is entering a decisive phase, where material science, industrial policy, and digital engineering intersect. Stakeholders that move quickly to leverage these trends stand to shape not only their own competitive futures, but also the trajectory of South Africa’s broader industrial transformation.

Top 5 Companies

1. Jushi Group

Jushi Group is one of the world’s largest producers of fiberglass and glass fiber reinforcements, supplying a broad spectrum of materials that underpin the Composites Market in South Africa. Headquartered in Tongxiang, China and founded in 1993, the company employs many thousands of people across manufacturing bases in China, Egypt, and other regions, and serves customers in more than 100 countries, including South Africa through regional distributors and trading partners. Its product portfolio relevant to the Composites Market in South Africa includes E-glass and ECR-glass rovings, chopped strands, mats, woven roving fabrics, and specialty reinforcements used in pipes and tanks, wind blades, marine, automotive, and building and construction applications. Jushi has expanded its geographic reach into Africa mainly via its large glass fiber plant in Egypt, which improves logistics and lead times for South African converters and OEMs. The company focuses on supply chain reliability, technical service, and cost-competitive high-volume reinforcements that are widely adopted by South African composite manufacturers in corrosion-resistant infrastructure, mining equipment, and transportation components. There are no widely reported recent mergers or acquisitions by Jushi Group that are specifically tied to the Composites Market in South Africa; its strategy in the region has primarily centered on export capacity expansion, local warehousing via partners, and strengthening relationships with South African distributors and fabricators to support growth in fiberglass-based composites.

2. CPIC

CPIC (Chongqing Polycomp International Corporation) is a leading global glass fiber manufacturer with a strong presence in industrial and infrastructure applications that are important to the Composites Market in South Africa. Established in 1991 and headquartered in Chongqing, China, CPIC operates multiple production bases in China and internationally, employing several thousand staff across manufacturing, R&D, and commercial operations. For the Composites Market in South Africa, CPIC’s core offerings include E-glass direct rovings, assembled rovings, chopped strands, continuous filament mats, combo mats, and fabrics designed for use in filament-wound pipes, GRP tanks, pultruded profiles, rebar, wind power components, and automotive applications. The company’s corrosion-resistant grades are particularly relevant for South Africa’s mining sector, chemical storage, and water infrastructure projects. CPIC has expanded geographically by building overseas plants in Europe and the Middle East and by leveraging trading hubs that support African markets, enabling shorter delivery times and more consistent supply to South African converters. While there are no widely documented mergers or acquisitions by CPIC that are directly linked to the Composites Market in South Africa, the company has focused on technical cooperation with global resin and sizing suppliers and on enhancing regional distribution networks to serve customers in Southern Africa. Its strategic emphasis on advanced sizing technology, application engineering, and cost-effective reinforcement solutions positions CPIC as a key supplier of fiberglass materials to South African composite manufacturers targeting infrastructure, energy, and transportation growth segments.

3. Taishan Fiberglass Inc.

Taishan Fiberglass Inc. (often referenced as CTG) is a major Chinese manufacturer of glass fiber and related composite reinforcement products that feed into a wide array of applications in the Composites Market in South Africa. Founded in 1997 and headquartered in Taian, Shandong Province, the company is part of China National Building Material Group (CNBM) and employs a large workforce across several production bases, with output exported to numerous countries worldwide including South Africa. Taishan’s product portfolio relevant to the Composites Market in South Africa includes E-glass rovings, chopped strands, stitched fabrics, mats, and high-performance specialty fibers used in wind energy, marine, sports and leisure, and automotive components, as well as in pipes, tanks, and construction panels. South African composite manufacturers source Taishan materials mainly through trading houses and regional distributors, benefiting from a broad range of cost-competitive reinforcement formats tailored for processes such as filament winding, pultrusion, vacuum infusion, and hand lay-up. The company has bolstered its geographic expansion by increasing export capacity, optimizing logistics routes via ports that efficiently serve Southern Africa, and enhancing technical support to international customers, which indirectly strengthens its footprint in South Africa. There are no widely publicized recent mergers or acquisitions directly tied to the Composites Market in South Africa involving Taishan Fiberglass Inc.; its growth strategy has largely emphasized capacity additions, process modernization, and product diversification, including reinforcements for renewable energy and infrastructure, sectors that align closely with South Africa’s ongoing investments in corrosion-resistant, lightweight composite solutions.

4. Toray Industries Inc.

Toray Industries Inc. is a diversified Japanese materials company and one of the global leaders in advanced composites, playing an important role as a technology and material supplier to high-performance segments of the Composites Market in South Africa. Established in 1926 and headquartered in Tokyo, Toray employs tens of thousands of people worldwide and operates production and R&D facilities in Asia, Europe, the Americas, and other regions. Toray’s composite-related portfolio relevant to the Composites Market in South Africa includes carbon fiber (Torayca), glass fiber, thermoset and thermoplastic prepregs, resin systems, and molded parts for aerospace, automotive, wind energy, sporting goods, industrial, and pressure vessel applications. South African customers typically access Toray materials through global aerospace and automotive supply chains, specialized distributors, and technology partnerships, particularly in high-end applications such as motorsport, defense, and advanced industrial structures. The company has expanded geographically through acquisitions and joint ventures in North America and Europe and through manufacturing sites that serve global OEMs, some of which are active in South Africa, thereby indirectly deepening Toray’s material penetration into the country. While there are no widely documented mergers or acquisitions by Toray that are specifically focused on the Composites Market in South Africa, its global M&A and partnership strategy in carbon fibers, aerospace materials, and automotive composites contributes to the availability of advanced Toray products to South African fabricators. Toray’s emphasis on lightweighting, sustainability, and next-generation composite technologies aligns well with emerging opportunities in South Africa’s transportation, renewable energy, and industrial upgrade projects.

5. Hexcel Corporation

Hexcel Corporation is a leading global supplier of advanced composite materials, particularly carbon fiber, honeycomb, and resin systems, and its technologies support multiple high-performance segments within the Composites Market in South Africa. Founded in 1948 and headquartered in Stamford, Connecticut, Hexcel employs several thousand people across manufacturing plants and R&D centers in North America, Europe, and the Asia-Pacific region. For the Composites Market in South Africa, Hexcel’s relevant portfolio includes aerospace-grade carbon fibers, prepregs, honeycomb cores, engineered fabrics, and structural adhesives that are utilized in aircraft structures, helicopters, defense platforms, high-end industrial components, and performance sports equipment. South African aerospace and defense programs, MRO operations, and niche industrial fabricators often access Hexcel products through global OEMs, licensed processors, and specialized distributors. The company’s geographic expansion has concentrated on co-locating production near major aerospace and wind energy hubs, along with technical centers that support downstream customers, which indirectly enhances supply reliability and technical support for South African users. There are no widely reported recent mergers or acquisitions by Hexcel that are explicitly targeted at the Composites Market in South Africa; however, its historic strategic actions, including technology collaborations and past M&A in aerospace composites, have broadened its product breadth available to South African markets. Hexcel’s focus on lightweighting, fuel efficiency, and advanced structural performance positions it as a key premium materials provider where South African industries require high-specification composite solutions in aviation, defense, and specialized industrial applications.

Table of Contents

List of Figures

List of Tables

Methodology

Lucintel has been in the business of market research and management consulting since 2000 and has published over 1000 market intelligence reports in various markets / applications and served over 1,000 clients worldwide. This study is a culmination of four months of full-time effort performed by Lucintel's analyst team. The analysts used the following sources for the creation and completion of this valuable report:

- In-depth interviews of the major players in this market

- Detailed secondary research from competitors' financial statements and published data

- Extensive searches of published works, market, and database information pertaining to industry news, company press releases, and customer intentions

A compilation of the experiences, judgments, and insights of Lucintel's professionals, who have analyzed and tracked this market over the years.

Extensive research and interviews are conducted across the supply chain of this market to estimate market share, market size, trends, drivers, challenges, and forecasts. Below is a brief summary of the primary interviews that were conducted by job function for this report.

Thus, Lucintel compiles vast amounts of data from numerous sources, validates the integrity of that data, and performs a comprehensive analysis. Lucintel then organizes the data, its findings, and insights into a concise report designed to support the strategic decision-making process. The figure below is a graphical representation of Lucintel's research process.

Buy Now

Choose a license that fits your team. Instant PDF delivery.

Prices exclude taxes. Instant delivery. Custom licensing available on request.

Frequently Asked Questions

What are the major drivers influencing the growth of the Composites Market in South Africa?

What are the major segments for Composites Market in South Africa?

Which Composites Market segment in South Africa will be the largest in future?

Do we receive customization in this report?

Key Questions

- • What are some of the most promising, high-growth opportunities for the Composites Market in South Africa by End Use Industry (Transportation, Marine, Wind Energy, Aerospace, Pipe and Tank, Construction, Electrical and Electronics, Consumer Goods, and Other End Use Industries), Manufacturing Process (Hand Lay-up, Spray-up, Resin Infusion (RRIM, RTM, VARTM), Filament Winding, Pultrusion, Injection Molding, Compression Molding, Prepreg Lay-up, and Other Manufacturing Processes), Molding Compound (SMC, BMC, and Thermoplastic Compounds ( SFT, LFT, GMT, CFT and Other)), Resin Type (Polyester, Epoxy, Vinyl ester, Phenolic, and Thermoplastics), Fiber Type (Glass Fiber, Carbon Fiber, and Aramid Fiber), Fiber Glass Product Form (Single End Roving, Multi End Roving, DUCs, Continuous Filament Mat, and Yarn), and Carbon Fiber Type (PAN Based Carbon Fiber and PITCH Based Carbon Fiber)?

- • Which segments will grow at a faster pace and why?

- • What are the key factors affecting market dynamics? What are the key challenges and business risks in this market?

- • What are the business risks and competitive threats in this market?

- • What are the emerging trends in this market and the reasons behind them?

- • What are some of the changing demands of customers in the market?

- • What are the new developments in the market? Which companies are leading these developments?

- • Who are the major players in this market? What strategic initiatives are key players pursuing for business growth?

- • What are some of the competing products in this market and how big of a threat do they pose for loss of market share by material or product substitution?

- • What M&A activity has occurred in the last 9 years and what has its impact been on the industry?

- • For any questions related to Composites Market in South Africa, Composites Market in South Africa Size, Composites Market in South Africa Growth, Composites Market in South Africa Analysis, Composites Market in South Africa Report, Composites Market in South Africa Share, Composites Market in South Africa Trends, Composites Market in South Africa Forecast, Composites Market Companies, write Lucintel analyst at email: helpdesk@lucintel.com. We will be glad to get back to you soon.